In an action seeking to establish that the defendant's property was burdened by an easement for water and sewer lines in favor of the plaintiff's property, evidence that until 1966 the plaintiff's and the defendant's property had been held in common ownership, that the use of the residences on the plaintiff's property required that water and sewer services be supplied through lines across the defendant's property, and that since 1950 the residences on the plaintiff's property had been served by such lines warranted the judge's conclusion that when the city of Boston took the property now owned by the plaintiff for nonpayment of taxes an easement by implication was created. [152]

The fact that title to a parcel of property passed as a result of a taking for nonpayment of taxes did not in itself preclude creation of an implied easement for water and sewer lines across remaining property of the taxpayer. [153-154]

CIVIL ACTION commenced in the Superior Court Department on April 6, 1979.

The case was heard by Jeremiah J. Sullivan, J., sitting under statutory authority.

James A. Paisley for the defendant.

James W. Stone for the plaintiff.

FINE, J. The parties, owners of adjoining parcels in Jamaica Plain, dispute whether the property of the defendant, Herbert Smith, trustee, [Note 1] is burdened by an easement for water and sewer

Page 150

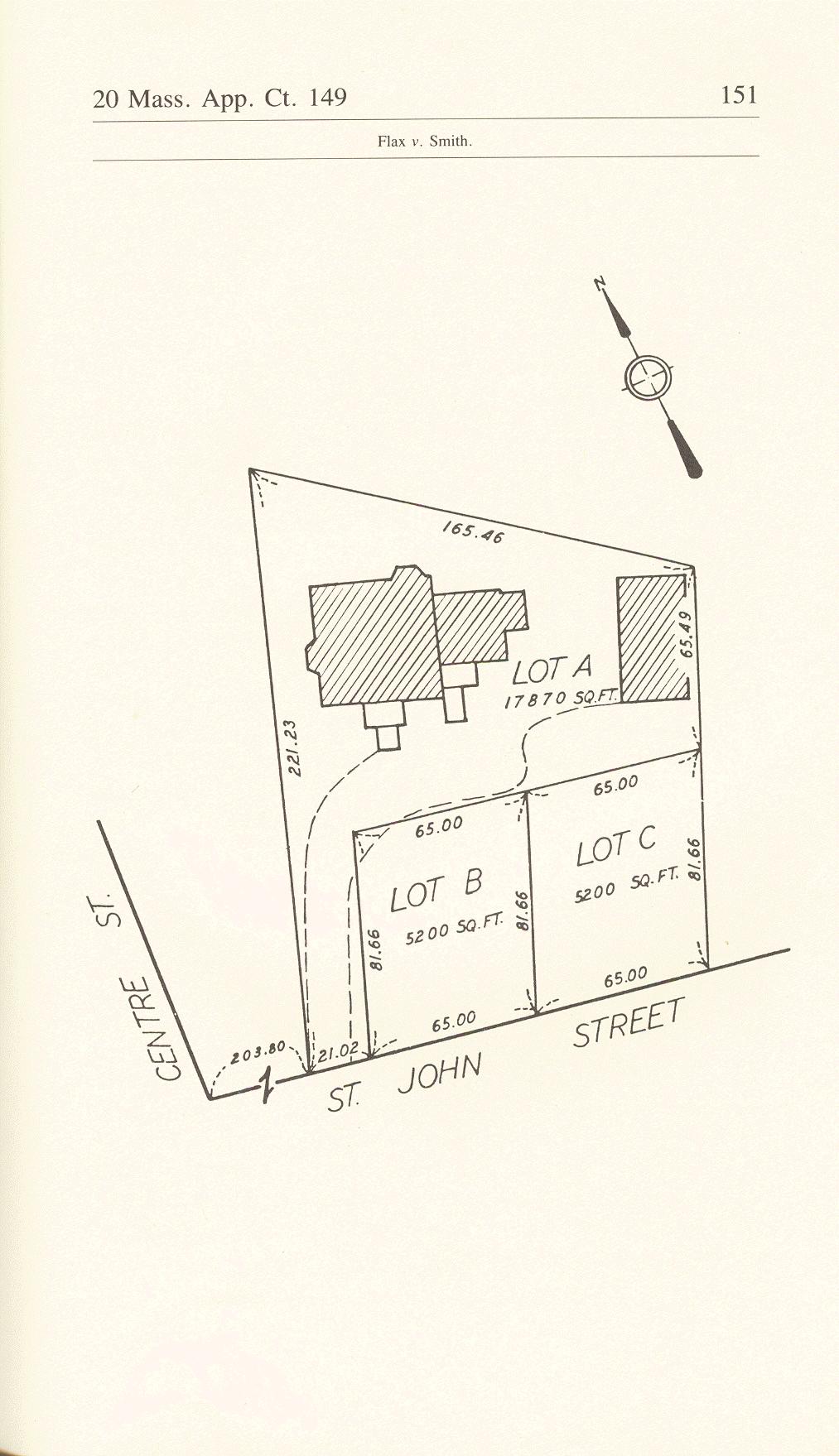

lines in favor of the property of the plaintiff, Steven Flax. After a trial without a jury, a Superior Court judge ruled that an easement by implication had been created, and he entered orders consistent with that ruling. [Note 2] The area is depicted on the accompanying diagram, the property owned by Flax being designated on the diagram as lot A and the property owned by Smith as lots B and C.

Lots B and C, fronting on St. John Street, contain five dwellings. Lot A, located to the rear of Lots B and C, contains two. Lot A is connected to St. John Street by a strip of land 21 feet wide and 150 feet in length. A hard surface driveway covers most of the strip. The residences on lot A are serviced by water and sewer lines, in existence, and in continuous use since 1950, which run under lot C from the main lines on St. John Street.

At all times prior to 1966, the parcels were in common ownership. In 1966, the city of Boston took lot A for nonpayment of taxes. See G. L. c. 60, Section 53, as amended by St. 1970, c. 85. The taking was confirmed by the Land Court in a 1974 decree. Flax acquired title from the city on August 29, 1978, having bid on the property at public auction. See G. L. c. 60, Section 43, as amended by St. 1935, c. 236. Smith's predecessor trustees obtained title to lots B and C in 1977 and promptly sought to prevent the easement.

The judge found, on the basis of the evidence, that between the residences on lot A and St. John Street there is rock ledge to a depth of three to ten feet, that sewer and water lines must be at least six feet deep to prevent freezing, and that the drilling and other work required to connect water and sewer lines from

Page 151

Page 152

the lot A residences directly to the main lines would cost $4,800, exclusive of the cost of the pipes and the connection. He concluded that there is a reasonable necessity for the claimed easement, and he ruled that when the city first acquired an ownership interest in 1966 it was the presumed intention of the city to take the property with the benefit of the existing water and sewer service. Accordingly, the judge determined that there was in existence an easement by implication.

No claim is made by Flax that he has an express easement or one obtained by prescription. See G. L. c. 187, Section 2. Thus, for Flax to prevail, he must bring his case within the authority recognizing implied easements. Such interests have been recognized when land was formerly in common ownership, when use of one part of the land was made for the benefit of another part up until the time of the severance of ownership, and when the use of one part is both reasonably ascertainable and reasonably necessary for the enjoyment of the other part. Mt. Holyoke Realty Corp. v. Holyoke Realty Corp., 284 Mass. 100 (1933). Sorel v. Boisjolie, 330 Mass. 513, 516 (1953). Cummings v. Franco, 335 Mass. 639 (1957). Perodeau v. O'Connor, 336 Mass. 472, 474-475 (1957). See Restatement of Property Sections 474 and 476 (1944). Park, Real Estate Law Section 276 (2d ed. 1981). As far as the respective use of the two parcels is concerned, the factual situations in both Cummings v. Franco and the illustration to comment c of Section 476 of the Restatement are remarkably similar to the factual situation in the instant case.

Unquestionably, apart from issues arising out of the particular way in which ownership passed from the grantor to the city, the plaintiff has brought himself within the class protected by the authority cited. The property was formerly in common ownership. The use of the residences on lot A required that water and sewer services be supplied through lines to the street. The services had been supplied by lines on the adjoining property since 1950. If the existence of the lines on his property was not actually known to the grantor, he could reasonably have ascertained the true facts. And, finally, reasonable necessity for continued use of the existing lines was established by the evidence.

Page 153

Smith contends that Flax failed to sustain his burden of proving the requisite intent for the creation of an easement by implication. Smith reasons that the grantor, parting with the property involuntarily as the result of a tax taking, did not intend to burden his remaining property (lots B and C) with the claimed easement. Smith is undoubtedly correct that the grantor, not having willingly conveyed anything to the city, did not actually intend to convey an easement. Thus, the issue is whether the fact that title passed involuntarily, pursuant to the tax title procedures (G. L. c. 60, Sections 37-60), changes what the result would have been had title passed by an ordinary voluntary conveyance.

To support his contention that the form in which title passed to lot A precludes the creation of an implied easement, Smith relies on language in those cases which suggests the importance of the grantor's intent. See Prentiss v. Gloucester, 236 Mass. 36, 52 (1920); Wellwood v. Havrah Mishna Anshi Sphard Cemetery Corp., 254 Mass. 350, 354 (1926). What is required, however, is not an actual subjective intent on the part of the grantor but a presumed objective intent of the grantor and grantee based upon the circumstances of the conveyance. See Restatement of Property Section 476 comment g (1944). One commentator has noted that "[t]hese fictional implications of `intent' are genuinely rooted in considerations of public policy." 3 Powell, Real Property par. 410, at 34-60 (Rohan rev. ed. 1984), citing Buss v. Dyer, 125 Mass. 287, 291 (1878).

In this case there are circumstances to consider even apart from the way the respective pieces of property were being used at the time of the taking. The effectiveness of the tax title procedures as a means of producing municipal revenue would be hindered if members of the public bidding on property at tax title auctions were to receive fewer rights than ordinary grantees of the same property. Such a rule would result in generally lower bids. The policy underlying the statutory tax title procedures has been stated as follows: "The importance of collecting taxes in order that governmental functions may be discharged is universally recognized. In the collection of taxes, the public interest requires that land be taken for nonpayment

Page 154

of taxes and sold under such circumstances that the necessary revenue may be obtained." See Napier v. Springfield, 304 Mass. 174, 177 (1939). See also Leigh v. Green, 193 U.S. 79, 89 (1904). Further, the grantor, a delinquent taxpayer, received a benefit from the conveyance since at least a portion, if not all, of his unpaid taxes were paid out of the proceeds of the sale, which proceeds presumably amounted to fair consideration. And the judge was quite correct in determining that one of the two parties to the transaction, the city, may be presumed to have intended to receive the benefit of the easement.

The recognition that an implied easement may arise out of a taking of property for nonpayment of taxes is not a departure from established law. Other types of involuntary conveyances have been held to result in the creation of implied easements. See Viall v. Carpenter, 14 Gray 126 (1859) (partition); Schmidt v. Quinn, 136 Mass. 575 (1884) (levy of an execution); 3 Powell, supra, par. 410, at 34-63, 34-64; Park, supra, Section 276, at 362. It may be, however, that the degree of necessity required must be greater than in the case of a voluntary conveyance. See Restatement of Property Section 474 comment b. Considering the importance of continued water and sewer services to occupants of residential property and the substantial construction work required to install new lines on lot A, even that higher degree of necessity has been shown in this case.

The other issues raised on appeal relate to the testimony of the expert witness upon whose opinions the judge found that the easement was reasonably necessary for the enjoyment of the use of lot A by Flax. The only objection to the testimony at trial was on grounds of relevance. Clearly the evidence was relevant. On appeal, for the first time, Smith contends that the witness lacked the qualifications necessary to provide such opinions. Even if the issue of the expert's qualifications were reviewable, no abuse of the judge's broad discretion could be shown.

Judgment affirmed.

FOOTNOTES

[Note 1] When the plaintiff commenced this action in 1979, Douglas D. Smith and Roger C. Smith were trustees for the Templeton Street Realty Trust and the Hosmer Street Realty Trust. Herbert Smith was substituted as the successor trustee for both trusts. For the sake of convenience, in the following we refer to the defendants as "Smith."

[Note 2] In his complaint, Flax sought an injunction restraining the defendants from interfering with his water supply, as well as damages for past interferences and a declaration that the defendants' lots were subject to easements for the water and sewer lines. The defendants counterclaimed, requesting an order directing Flax to stop using the lines and to pay for past use. In addition to declaring that an easement existed, the court enjoined Smith from interfering with Flax's reasonable use of the easement, ordered that Flax and Smith share the cost of water and sewer charges, and ordered Flax to install and maintain meters to measure actual water usage.