This cause came on to be heard upon the plaintiff's complaint filed October 30, 1987 as amended November 6, 1987 under G.L. c. 240, §6-10 to quiet title to certain real estate situated in Oak Bluffs, Dukes County, Massachusetts. The plaintiff claims record title to nineteen parcels of vacant land located in a subdivision known as "Bellevue Heights" shown on a plan by T. C. Luce dated June 22, 1876, recorded with the Dukes County Registry of Deeds, Plan Book 4, Page 5. The plaintiff's claim is through the heirs of one Rodman as set forth below. Each parcel is approximately 50 x 100 feet in size. These parcels are referred to herein collectively as "property." Each of the defendants claims ownership to one or more parcels by virtue of various deeds which flow from a tax taking by the Town of Oak Bluffs in 1940 for the nonpayment of taxes which were assessed to the "Estate of Frank C. Smith." The defendants also claim title to the parcels and to portions of certain ways on said plan by adverse possession.

A trial was held on April 4 and April 5, 1988 at Edgartown at which a stenographer was sworn to record and transcribe the testimony. The property was viewed on April 15, 1988. Ten witnesses testified and thirtytwo exhibits were introduced into evidence, which exhibits are incorporated herein for the purpose of any appeal.

I find the following:

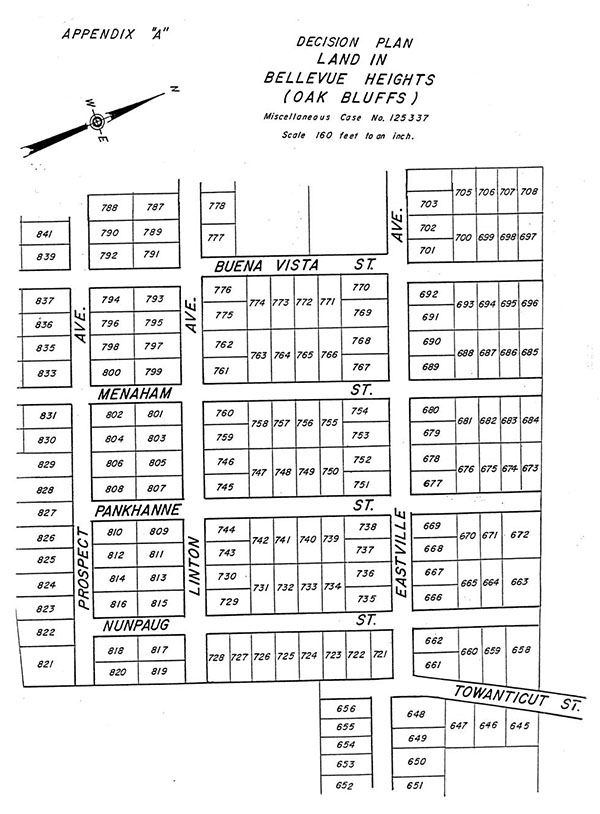

1. On June 22, 1872, T. C. Luce recorded a plan with the Dukes County Registry of Deeds [Note 1] of a subdivision to be known as "Bellevue Heights" in what is now the Town of Oak Bluffs. The plan locates the property only as "Martha's Vineyard" ("1872 plan"). A portion of the plan showing the lots in question has been reproduced and is attached hereto as Appendix "A."

2. On June 13, 1876, the trustees in bankruptcy for T. C. Luce transferred title to the land in the Bellevue Heights development to Francis C. Smith by deed recorded at Book 73, Page 312.

3. On March 30, 1895, Francis C. Smith transferred all of his right title and interest in and to any and all real estate situated in the County of Dukes to Edmund Rodman.

4. On June 6, 1895, the Smith to Rodman deed was recorded at Book 93, Page 199. The Grantor Index at the Registry covering the years 1859 to 1895 contains the following entry: Time of Reception "1895 June 6" Grantors "Smith, Francis C." Grantees "Edmund Rodman" Town where the lands lie "Dukes County, Edgartown" Book "93", Page "199." The plaintiff's claim of title is from the heirs of said Rodman.

5. Edmund Rodman died May 7, 1902. His will makes no specific mention of real estate nor does his inventory. None of the estates in the plaintiff's alleged chain from 1902 to date contain wills or inventories referencing subject property. Neither is there any evidence of either Rodman or his heirs ever visiting the property or paying any taxes thereon.

6. At no time has there been any attempt to survey the property or to lay out or mark out in any fashion the "paper streets" shown on the 1872 plan as crossing the property.

7. The records of the assessor in the Town of Edgartown reflect notification by the Dukes County Registry of the 1895 conveyance from Smith to Rodman. The records of the tax assessor in the Town of Oak Bluffs do not reflect such notification, and apparently Francis C. Smith remained the owner of the Bellevue Heights Land on the tax record of the Town of Oak Bluffs.

8. On or about August 30, 1940, the collector of taxes for the Town of Oak Bluffs made a tax taking of certain land in the Bellevue Heights development, specifically Lots 722-734 and Lots 813-820, pursuant to the procedure for foreclosing land of low value, G.L. c. 60, §§53 and 54. Francis C. Smith was listed as the person assessed taxes for the 1938 tax year in the Instrument of Taking, the Affidavit to Foreclose Tax Title of Low Value and the Treasurer's Deed to a Person, Land of Low Value.

9. On May 5, 1943, a Treasurer's Deed to a Person, Land of Low Value conveyed the Bellevue Heights property to Eben D. Bodfish. The defendants named herein are record owners under that chain of title of the 19 lots in dispute.

10. The instrument of tax taking dated May 24, 1943 was recorded at Book 202, Page 223.

11. On September 2, 1957, Dr. Leon H.S. Thomas and Marion Thomas purchased Lots 727-730 and 813-820 in the Bellevue Heights development, Oak Bluffs, by deed recorded at Book 233, Page 445. [Note 2]

12. On February 16, 1959, Dr. and Mrs. Thomas purchased Lots 725 and 726 in the Bellevue Heights development by deed recorded at Book 236, Page 378.

13. At the time of the purchase of these lots by Dr. and Mrs. Thomas, the land was wooded with a small cottage on Lots 727 and 728. In 1958, the Thomases expanded the cottage into a large home appropriate for use on a year round basis. The expansion extended onto what is shown on the plan as Nunpaug Street and a portion of Lot 729.

14. The lots purchased by Dr. and Mrs. Thomas, from present on-site appearance, and as used by them, appear to be a single parcel of land bounded on the east by an unpaved road, Towanticut Street, and on the south by an unpaved road, Prospect Avenue, both having somewhat irregular side lines. The westerly and northerly boundaries are not marked by boundary markers, although at all relevant times the Thomases and their neighbors, the Nixes, agreed upon the location of their respective property lines.

15. From 1958 to 1983, the Thomases spent every summer on the property. Since 1983, Mrs. Thomas has lived on the property year round. In May, Mrs. Thomas would open up the property for the season and in June, the property would be rented out. After school recessed for the summer, Mrs. Thomas and her three children would spend July and August on the property. Dr. Thomas would join them for the month of August. On Labor Day, the property would be closed for the season. Dr. Thomas died in 1978; however, Mrs. Thomas and the children continued to summer at Oak Bluffs.

16. In 1963, the Thomases cleared portions of the property and created a "horseshoe" shaped driveway, a yard and a garden. This work encompassed portions of Lots 729, 730, 813, 815, 817, 819 and portions of what is shown on the plan as Nunpaug Street and Linton Avenue. Portions of Lots 729 and 730 were filled in at this same time. In 1967, a clearing was made on Lot 817 for parking cars and sometime in the early 1960's, a septic tank was put on Lot 729.

17. The Thomases left a portion of the property facing Towanticut Street in a semi-wooded state for privacy. From 1958 to the present, the Thomases cleared these areas of brush, dead wood and fallen trees, sprayed for caterpillars, gypsy moths and mosquitoes and planted additional bushes and trees on the property. From the years 1971 to 1983, the Thomases cut firewood from the property and between 1971 and 1978 allowed their children and their friends to camp on the property. Each year from 1958 to 1971, Dr. Thomas walked the boundaries of his property and at various times hired gardeners to maintain the land and the areas surrounding the house.

18. From 1958 to the present, the Thomas family used a path through the wooded area on their property crossing Lots 818, 816 and 813 to walk to a nearby relative's property.

19. From 1957 to the present for Lots 727-730 and Lots 813-820 and from 1959 for Lots 725-726, the Thomases have paid taxes on the property.

20. On July 2, 1962, Ida A. Nix purchased Lots 722-724 in the Bellevue Heights development by deed recorded at Book 245, Page 279.

21. On September 21, 1965, Ida A. Nix purchased Lots 731-733 in the Bellevue Heights development by deed recorded at Book 258, Page 411.

22. On July 7, 1966, Ida A. Nix purchased Lots 734 and 735 in the Bellevue Heights development by deed recorded at Book 263, Page 11.

23. On August 31, 1972, Ida A. Nix conveyed Lots 731-733 and 734-735 to Andrew W. Nix, Jr., Gertrude C. Nix, Phenoris N. Young, Vivian C. Nix and Beverly R. Johnson by deed recorded at Book 301, Page 5.

24. On or before 1964, Ida Nix had the property surveyed and built a house on Lots 721 and 722. Portions of Lots 723 and 724 were cleared and used as a backyard.

25. From 1964 to the present, Mrs. Nix has spent every summer at the property and has been accompanied by friends, children and grandchildren every summer.

26. The Nix family has left some of the lots in their natural state for privacy, yet have often cleared the area including the adjacent section of Nunpaug Street of dead trees and brush. Since 1964 to the present, the Nix family has used Lots 722, 723 and 724 and a portion of Nunpaug Street as one lot for various activities including planting grass and flowers, clearing trees, raking leaves, hiking, picnicking, camping in tents and playing volleyball and croquet. Since 1965 to the present, the Nix family has utilized Lots 731, 732, 733 and 734 as an extension of the backyard to the house and have cleared trees and brush from these lots annually.

27. In 1972, Ida Nix conveyed Lots 731-734 to her son, Andrew W. Nix, Jr., his wife and daughters, Gertrude C. Nix, Phenoris N. Young, Vivian C. Nix and Beverly R. Johnson. The Nix family has continuously used these lots, along with Lots 721-724, for summer activities.

28. From 1965 to the present, the Nix family has walked paths throughout Lots 721-724 and 731-734 to, reach the boundaries of their property and the various abutting streets. Many of the paths throughout the property were used to reach Mrs. Nix's son's home located a short distance away.

29. Mrs. Nix had nineteen pine trees and stumps removed from the lots and erected a screenhouse in the summer for protection from mosquitoes. Every year, the family would pick up trash along the boundary of the lots facing Eastville Avenue. Picnic tables were placed behind the house in the shade of the trees. A swing set was on the property for the younger children and was recently removed because it had rusted over the years.

30. Every year since the purchase of the lots in 1962 and 1965, Ida Nix or Andrew W. Nix, Jr. has paid the taxes on Lots 721, 722, 723, 724, 731, 732, 733, 734 and 735.

The plaintiff herein has the burden of establishing his title not simply by demonstrating weaknesses or nonexistence of the defendants' title, nor by merely demonstrating a better title than the defendants possess, but by demonstrating and proving sufficient title to succeed in his action. Sheriff's Meadow Foundation, Inc. v. Bay-Courte Edgartown, Inc., 401 Mass. 267 , 269 (1987).

The plaintiff is an attorney admitted to practice in the states of both New York and Connecticut but not, however, in Massachusetts. He presents certain documents which, if complete and credible, could establish a 3/4 interest in the disputed properties. The plaintiff did not present himself, or anyone else, as a witness expert in the field of land titles. It may be true as he argues that such expert testimony is not required, however, in such instance the evidence presented via the exhibits must clearly and unequivocally support his claim absent any reasonable inference to the contrary, or that other documentation may as likely exist which would defeat such claim. The plaintiff's claim is based on numerous documents introduced at trial together with voluminous documents filed post-trial by letter of April 14, 1988 and without objection by opposing counsel. While said documentation may support the plaintiff's claim, such determination would, in essence, require this Court itself to conduct a rather complete title search. This is not the function of the Trial Court not even the Land Court Department thereof. If it were, parties might well begin to offer the entire records of a registry and rest their case without further explanation. This is what, in effect, the plaintiff has done. Hence, while the plaintiff's exhibits may support his claim, I decline to make such finding absent competent testimony to that effect.

Notwithstanding the foregoing, I find that the defendants, Thomas and Nixes, have acquired title to the property as described above, including those portions of Nunpaug Street and Linton Avenue as are bounded by the property, by adverse possession and under the color of title doctrine.

Considering the nature and topography of the properties, the nonpermissive activities of the Thomases and Nixes have been actual, open, notorious, exclusive and adverse for the requisite period prior to the filing of this action to meet the standards of Ryan v. Stavros, 348 Mass. 251 , 262 (1964).

While it is true that for the most part the use of the property has been seasonal and the use varied from time to time, the defendants need not prove continuous use of every segment of the land claimed for the entire statutory period. Their actual use and enjoyment of the properties such have been as the average owner of similar property would use and enjoy it so that persons residing in the neighborhood would be justified in regarding the defendants as exercising the exclusive dominion and control incident to ownership. Such activity is sufficient to establish ownership by adverse possession. Shaw v. Solari, 8 Mass. App. Ct. 151 , 156-157 (1979); Mahoney v. Heebner, 343 Mass. 770 (1961).

The nature and extent of occupancy required to establish rights by adverse possession vary with the character of the land, the purposes for which it is adapted and the uses to which it has been put. Kershaw v. Zecchini, 342 Mass. 318 , 320 (1961). While both parcels have considerable growth when viewed as a whole, both contain well maintained dwelling houses and, for the most part, have been cleared of much underbrush. At least when visited in early April, it was possible to see across both parcels. Accordingly, the lands do not constitute "wild land" or woodland so as to require the rather strict activities of Cowden v. Cutting, 339 Mass. 164 (1959) to establish possession.

I further find that even had the defendants' activities over the entire parcels been insufficient to establish adverse possession, they have so established their title under the doctrine of "color of title" by the construction of improvements and dwellings on the land. As noted, the plaintiff is not claiming title to the individual parcels on which he believes the dwelling, or a part thereof, at least are located. This exclusion does not, however, defeat the defendants' claim under either theory. Norton v. West, 8 Mass. App. Ct. 348 , 350-351 (1974). I do not consider the "paper streets" a hindrance in such finding inasmuch as they originate on an 1872 plan, have never been used or even laid out on the ground and do not appear to be necessary to provide access to a public way to any abutter.

In any event, it is clear that the use of the premises by the defendants has been such as to put the true owner on notice of the hostile

activity of the possessors so that he, the owner, may have had an opportunity to vindicate his rights by legal action. Ottavia v. Savarese, 338 Mass. 330 , 333 (1959); Dow v. Dow, 243 Mass. 587 , 593 (1923).

In consideration of the foregoing, I find and rule that the plaintiff has failed to meet his burden of proving that the interests which he may have acquired from the heirs of Edmund Rodman give him any title to the property of the defendants and that his suit is dismissed.

There have been filed reports for findings of fact which I have considered. Certain requests have been granted and are contained herein.

I have taken no action on the remainder as I have made my own findings as to the facts I find pertinent.

Judgment accordingly.

RONALD L. MONTEROSSO, individually and as administrator of the Estate of John Titcomb, deceased and Margaret Titcomb Urquhart, deceased vs. MARION O. THOMAS, ANDREW W. NIX, JR., GERTRUDE C. NIX, PHENORIS N. YOUNG, VIVIAN C. NIX, IDA A. NIX and BEVERLY R. JOHNSON.

RONALD L. MONTEROSSO, individually and as administrator of the Estate of John Titcomb, deceased and Margaret Titcomb Urquhart, deceased vs. MARION O. THOMAS, ANDREW W. NIX, JR., GERTRUDE C. NIX, PHENORIS N. YOUNG, VIVIAN C. NIX, IDA A. NIX and BEVERLY R. JOHNSON.