A draft on an insurance company, signed by one designating himself as assistant superintendent of the company, payable through a certain bank "upon acceptance" by the company, was not a negotiable instrument.

An assignee of a contract of conditional sale of an automobile, who had indorsed a draft, issued by an insurer for an amount admittedly due under a policy of collision insurance and payable to the vendee and such assignee subject to certain formalities prescribed for the benefit of the insurer, where such indorsement was below a provision acknowledging receipt of the amount stated in the draft in full settlement and discharge of the claim under the policy, and who had left the draft, so indorsed, in the possession of the vendee although, because he doubted the vendee's integrity, he had asked the insurer not to pay it, was not entitled to rely on noncompliance with the formalities prescribed in the draft and was estopped to contend that such amount, admittedly due, should not be paid to one who had received the draft from the vendee, bearing the vendee's indorsement also, and had paid the vendee money therefore relying on the indorsements.

BILL IN EQUITY, by amendment from an action at law begun by writ in the Superior Court dated May 5, 1943.

The case was heard by Donnelly, J.

The defendant Eastern Finance Corporation did not set up a counterclaim in its answer.

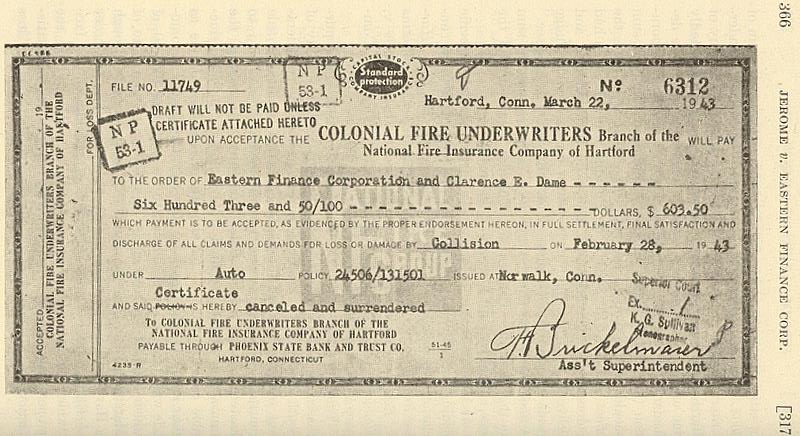

A reproduction of the draft described in the opinion appears on page 366.

Although both defendants appealed from the decree entered in the Superior Court, only the appeal of Eastern Finance Corporation was argued in this court.

C. W. Proctor, for the defendant Eastern Finance Corporation.

W. J. Griffin, for the plaintiff.

WILKINS, J. This is a suit in equity to reach and apply

Page 365

in satisfaction of a debt of the defendant Dame the sum of $603.50 in the hands of the defendant Colonial Fire Under-writers Branch of the National Fire Insurance Company of Hartford (hereinafter called Colonial) which was admittedly due under an automobile collision policy issued to the defendant Dame. The defendant Eastern Finance Corporation (hereinafter called Eastern) contended that this sum should not be paid to the plaintiff. There is in issue the effect of a draft for $603.50 on Colonial which Eastern had indorsed and delivered to Dame, who then indorsed and delivered it to the plaintiff in return for cash. The judge made a voluntary "finding of fact and order for decree." A final decree was entered ordering Colonial to pay the sum to the plaintiff. Eastern and Colonial appealed, and the case is here without a report of testimony.

It is open to the defendants to argue that the specific findings of the judge necessarily preclude his general conclusion. Birnbaum v. Pamoukis, 301 Mass. 559, 562. Harlow Realty Co. v. Whiting, 308 Mass. 220, 223-224. Wilkins v. Berkeley Realty Corp. 311 Mass. 148, 151. Searls v. Standard Accident Ins. Co. 316 Mass. 606, 607, 610. Compare Druker v. Druker, 308 Mass. 229, 230.

These findings were: On February 25, 1943, Dame purchased an automobile from the Simons Sales Company of South Norwalk, Connecticut, and as part of the consideration executed a note for $1,271.85 and a conditional sale contract, which for value were immediately assigned to Eastern by the Simons Sales Company. As part of the transaction Dame procured from Colonial "a $50 deductible collision policy," payable to Eastern and Dame as their interests might appear. On February 28 the automobile was damaged in a collision to the extent of $653.50, of which $603.50 was due under the policy. Under date of March 22, 1943, Colonial made out a draft, payable through a Hartford bank, on acceptance by Colonial, to the order of Eastern and Dame for $603.50, reciting on its face "which payment is to be accepted, as evidenced by the proper endorsement hereon, in full settlement, final satisfaction and discharge of all claims and demands for loss

Page 366

Page 367

or damage by Collision on February 28, 1943 under Auto policy 24506/131501 issued at Norwalk, Conn. and said Certificate is hereby canceled and surrendered." Stamped on the face was "Draft will not be paid unless certificate attached hereto." The certificate referred to was one given Dame as evidence of the fact that the automobile was insured under a blanket policy issued by Colonial to Eastern. At no time was it attached to the draft. The space for acceptance by Colonial was left blank. On March 23 Eastern received the draft by mail from Colonial, and on that day Dame went to Eastern's office at Hartford. The treasurer of Eastern, one Mintz, indorsed below a provision reading, "In endorsing this draft I/We hereby acknowledge receipt of the amount hereof, in full settlement, final satisfaction and discharge of all claims and demands against the Colonial Fire Underwriters Branch of the National Fire Insurance Company of Hartford, for loss and damage of the date and under the policy indicated on the face hereof." Dame left with Eastern a new collision policy of the Pacific Fire Insurance Company (hereinafter called Pacific), which he had been told he must procure in accordance with his agreement with Eastern. Mintz turned over the indorsed draft to Dame on the understanding that Dame would use it to pay a bill for repairing the automobile to one Fleming in Worcester. Later on March 23, after Dame had left, Eastern not only learned that Pacific was to cancel its policy, but also acquired other information about Dame which raised doubt as to whether the draft would be used to pay the repair bill. Mintz at once asked Colonial not to pay the draft, and notified Fleming not to turn the automobile over to Dame unless Mintz was present. On March 25 Mintz met Dame at Fleming's garage, and informed him he would have to get a new policy to replace the one on which a five-day notice of cancellation had been given by Pacific on March 24. Mintz paid Fleming $653.50, and drove the automobile to Hartford. Thereupon, Dame, knowing that the automobile was to be repossessed by Eastern and that the draft would not be accepted when presented, went to the plaintiff, and represented

Page 368

that it was a valid claim which would be paid upon presentation, indorsed the draft, and got $603.50 from the plaintiff in exchange for it. The judge "found" that by reason of restrictions as to payment the draft was not a negotiable instrument; that it was not a chose in action upon which recovery could be had without acceptance by Colonial; that it never became a complete and operative contract; and for these reasons ruled that the plaintiff could not recover "by virtue of the draft." He found that Colonial admitted holding $603.50 which was due under the policy, and concluded: "Since Eastern released and discharged Colonial in writing by endorsing the release of all its rights against Colonial which was printed on the back of the draft and by that writing misled the plaintiff into paying $603.50 to Dame, Eastern should not now be entitled equitably to withdraw the release which misled the plaintiff to his detriment and assert rights in the fund in the hands of Colonial. Either the plaintiff or Eastern must suffer the loss of the $603.50 in the hands of Colonial and since Eastern by endorsing the release on the back of the draft enabled Dame to perpetrate a fraud on the plaintiff, I find that the equities in the fund are with the plaintiff and that Eastern is estopped by its conduct in claiming the fund in the hands of Colonial as against the plaintiff."

No contention is made that the law of Connecticut differs in any material respect from the law of this Commonwealth.

The ruling that the draft was not a negotiable instrument was right. "An instrument to be negotiable . . . must contain an unconditional promise or order to pay a sum certain in money." G. L. (Ter. Ed.) c. 107, Section 23, cl. 2. Conn. Gen. Sts. (1930) Section 4318. Here liability was made conditional upon acceptance. Berenson v. London & Lancashire Fire Ins. Co. 201 Mass. 172. This is apart from the requirement that a certificate be attached.

The decree for the plaintiff, based upon the finding that there was an estoppel, must stand. "Whether an estoppel has been established usually presents an issue of fact." Stern v. Lieberman, 307 Mass. 77, 82, and cases cited.

Page 369

National Development Co. v. Gray, 316 Mass. 240, 251. Nothing in the findings inescapably forbids such a conclusion. Dame and Eastern on the face of the draft were jointly entitled. After voluntary indorsement Eastern confided to Dame sole possession of the draft, which then bore acknowledgment of full satisfaction of all claims Eastern had arising out of damage to the automobile. See Shaw v. Victoria Coach Line, Inc. 314 Mass. 262, 265. Dame, as one payee of the draft indorsed in blank by the other payee, was with Eastern's consent placed in a position where he was clothed with the apparent right to dispose of the draft, subject, of course, to the right of Colonial to withhold acceptance. We think that the applicable principles are those to be found in Herman v. Connecticut Mutual Life Ins. Co. 218 Mass. 181, 185, 186, a case concerning a policy of life insurance, where it was stated, "we have here to do, not with a chattel, but with a non-negotiable chose in action, the right to receive in the future a certain sum of money upon the happening of certain contingencies. . . . The court must apply here the rule stated by the Chief Justice in Baker v. Davie, 211 Mass. 429, 440, `that when an owner has so acted as to mislead a third person into the honest belief that the one dealing with the property had the right to do so, he is estopped from showing the truth.' . . . But this estoppel of a rightful owner to set up his title against a bona fide purchaser for value from one who had not the right to sell rests upon the conduct of the rightful owner. It arises against him when by his own conduct he has so clothed the wrongdoer with the indicia of ownership as to justify third persons in regarding the wrongdoer as either the rightful owner or as having authority from that owner. The estoppel arises only from the owner's voluntary action tending to produce and in fact producing that result." In Scollans v. E. H. Rollins & Sons, 179 Mass. 346, 353, it was said by Chief Justice Holmes with respect to certificates of indebtedness of a city payable to a named payee and transferable only at the city treasurer's office, "if the owner of the instrument intrusts it to another, he does so charged with notice of the power to deceive

Page 370

which he is putting into that other's hands, and if deception follows he must bear the burden." This is not in any way on the ground that the draft became a negotiable instrument, for it did not, but is wholly on the ground of estoppel. Baker v. Davie, 211 Mass. 429, 436. Ironside v. Levi, 278 Mass. 18, 22. Eastern knew that it was "making actual deceit possible." Edgerly v. First National Bank, 292 Mass. 181, 183. "Upon these facts . . . `the principles which underlie equitable estoppel place the loss upon him whose misplaced confidence has made the wrong possible.' National Safe Deposit, Savings & Trust Co. v. Hibbs, 229 U.S. 391, 397." Loring v. Goodhue, 259 Mass. 495, 498. Russell v. American Bell Telephone Co. 180 Mass. 467, 469-470. Gardner v. Beacon Trust Co. 190 Mass. 27, 28-30. Tower v. Stanley, 220 Mass. 429, 437. New York Life Ins. Co. v. Brown, 99 Fed. (2d) 199, 202. McNeil v. Tenth National Bank, 46 N. Y. 325. Moore v. Metropolitan National Bank, 55 N. Y. 41. The absence of any finding as to a business usage or custom to assign such a draft is of no consequence.

The fact that the certificate was not attached, or the fact, if it be a fact, that the draft was not accepted, does not assist Eastern. These formalities were prescribed for its own benefit by Colonial, which, as we view the finding, now stands ready to pay the amount to such party as is determined to be entitled thereto. Abbruzise v. Sposata, 306 Mass. 151, 153-154, and cases cited. The present case is distinguishable from Berenson v. London & Lancashire Fire Ins. Co. 201 Mass. 172, where the insurance company denied that there had been any binding adjustment of the loss. Here Colonial stands in effect as a stakeholder of a sum admittedly due. It is not open to Eastern, which enabled Dame to defraud the plaintiff, either to set up conditions available exclusively to Colonial, which Colonial could, and on the findings did, waive; or to assert that all was a nullity until the moment when Colonial might consent formally and absolutely to be bound. Eastern took the risk that Colonial might not insist upon the conditions and might choose to recognize the obligation. Moreover, even

Page 371

after Eastern had begun to doubt Dame's integrity, it apparently took no precaution to regain possession of the draft. See Herman v. Connecticut Mutual Life Ins. Co. 218 Mass. 181, 187.

There is nothing in Moore v. Spiegel, 143 Mass. 413, Dallinger v. Richardson, 176 Mass. 77, 83, Commercial National Bank v. Bemis, 177 Mass. 95, 99, Laprade v. Fitchburg & Leominster Street Railway, 205 Mass. 77, 79, or Cleaveland v. Malden Savings Bank, 291 Mass. 295, 297-298, in conflict with what we have herein held.

It would not be profitable to make further analysis to determine whether the plaintiff should prevail on the draft itself or on general equitable principles, nor do we consider the correctness of the ruling "that the plaintiff cannot recover by virtue of the draft." The judge's ultimate conclusion that the plaintiff was entitled to recover, if not required, at least is not necessarily precluded, by his other findings.

Decree affirmed with costs.