In June 2018, Dr. Manhui Liu (then trustee of the 389 Main Street Trust) sued defendant Mystery, LLC and the defendant Trustees of the City Center Office Condominium (the "Condominium Trustees"; together with Mystery, the "Defendants"). Liu is a dentist, and she operates her practice from what is advertised as Unit 204 of the City Center Office Condominium in Malden, Massachusetts (the "Condominium"). Liu is the owner of Unit 204.

In her first amended complaint, Dr. Liu sought a declaration that the boundary between Unit 204 and Mystery's abutting unit, Unit 202, is as set forth in the Condominium's Master Deed (the "Deeded Boundary"). The Master Deed dates from 1983. Liu asked for an injunction directing Mystery to remove allegedly encroaching walls (the "Demising Walls") from Unit 204, as the Demising Walls don't run along the Deeded Boundary. She also sought a declaration that Unit 204's beneficial interest in the Condominium is as set forth in the original Master Deed.

In November 2018, Mystery and the Condominium Trustees separately answered Dr. Liu's amended complaint. Their chief defense is that when Liu purchased Unit 204, in 2007, she assented to two amendments to the Master Deed. Defendants argue that the amendments made the location of the Demising Walls the boundary between Units 202 and 204 (the "Disputed Units") and assigned to the Disputed Units new beneficial interests in the Condominium.

In June 2019, Dr. Liu moved for summary judgment on her claims. The Court denied that motion, as the facts concerning her alleged 2007 ratification of the changes to the dimensions of the Disputed Units and their beneficial interests were in dispute. The Court also held that the immediate prior owner of the Disputed Units, Breton LLC, may have retained title to the parts of Unit 204 (as determined by the original Master Deed) that the Demising Walls had physically severed from the rest of Unit 204 and, from all appearances, made part of Unit 202 (the "Detached Area").

At the Court's direction, Dr. Liu amended her complaint to add Breton as a defendant. Defendants each answered that complaint. Mystery also cross-claimed against Breton, seeking a deed to Unit 202 that included the Detached Area. Breton appeared in the case but didn't answer either Liu's Second Amended Complaint or Mystery's cross-claim. Instead, in July 2020, Breton executed a deed purporting to confirm its earlier grant to Mystery of whatever right, title and interest Breton had in original Unit 202 as well as the Detached Area. As Mystery had thus succeeded to Breton's interests in the Detached Area, Mystery also succeeded to Breton's status as a party defendant for purposes of Liu's claims against Breton for that Area. The Court thus dismissed Breton as a party defendant. Mystery dismissed its cross-claim against Breton too.

In January 2021, counsel for Dr. Liu withdrew his appearance. The parties appeared for trial on February 8 and 9, 2021, by Zoom videoconference. Liu represented herself at that trial. The Court conducted a view of the Disputed Units prior to receiving testimony. Having heard and seen the parties' witnesses, having reviewed the exhibits admitted into evidence, having viewed the Disputed Units, and having heard the arguments of Dr. Liu and counsel for Mystery and the Condominium Trustees, the Court FINDS the facts set forth above as well as those that follow. [Note 1]

1. The Condominium was established in 1983 pursuant to the Master Deed. The Master Deed is recorded at the Middlesex South Registry of Deeds (the "Registry").

2. Exhibit B to the Master Deed ("Exhibit B") recites the shares of beneficial interests originally assigned to each unit in the Condominium.

3. Also recorded with the Master Deed was a set of floor plans depicting the layout and boundaries of the units (the "Floor Plans").

4. The City Center Office Condominium Trust (the "Trust") was established at the same time as the Condominium, as the organization of the Condominium's unit owners. The Trust was created under a Declaration of Trust that's recorded at the Registry.

5. The Master Deed, Exhibit B, and the Floor Plans originally called today's Unit 204 (ignoring the effects of the Demising Walls) "Unit 201." As Finding #16 below notes, in May 2004, original Unit 201 was re-named Unit 204.

6. Prior to 1999, there was no wall or other physical division between the Disputed Units. They formed a single physical space. The Disputed Units nevertheless were two separate units for purposes of the Master Deed. Page 2 of the Floor Plans, labeled "Second Floor Plan," shows the Deeded Boundary between the Disputed Units. Because the Disputed Units then formed a single space, the Second Floor Plan shows the Deeded Boundary as a broken or dashed line.

7. Exhibit B attributes to each Condominium Unit separate shares of beneficial interests in the Condominium and its common areas. Exhibit B describes Unit 204 (then called Unit 201) as having 1,569 square feet of area, and a 6.6842% share of the beneficial interests in the Condominium. Exhibit B describes Unit 202 as having 1,425 square feet of area, and a 5.8148% share of the beneficial interests. Together, according to Exhibit B, the Disputed Units have 2,994 square feet of area and a 12.499% share of the beneficial interests in the Condominium.

8. Section 5(b) of the Master Deed acknowledges there were unseparated Units within the Condominium. Section 5(b) states that "[w]hen such interior common walls are actually constructed, a floor plan showing such actual construction shall be recorded as a special amendment to this Master Deed pursuant to Section 17(b)(i) . . . ."

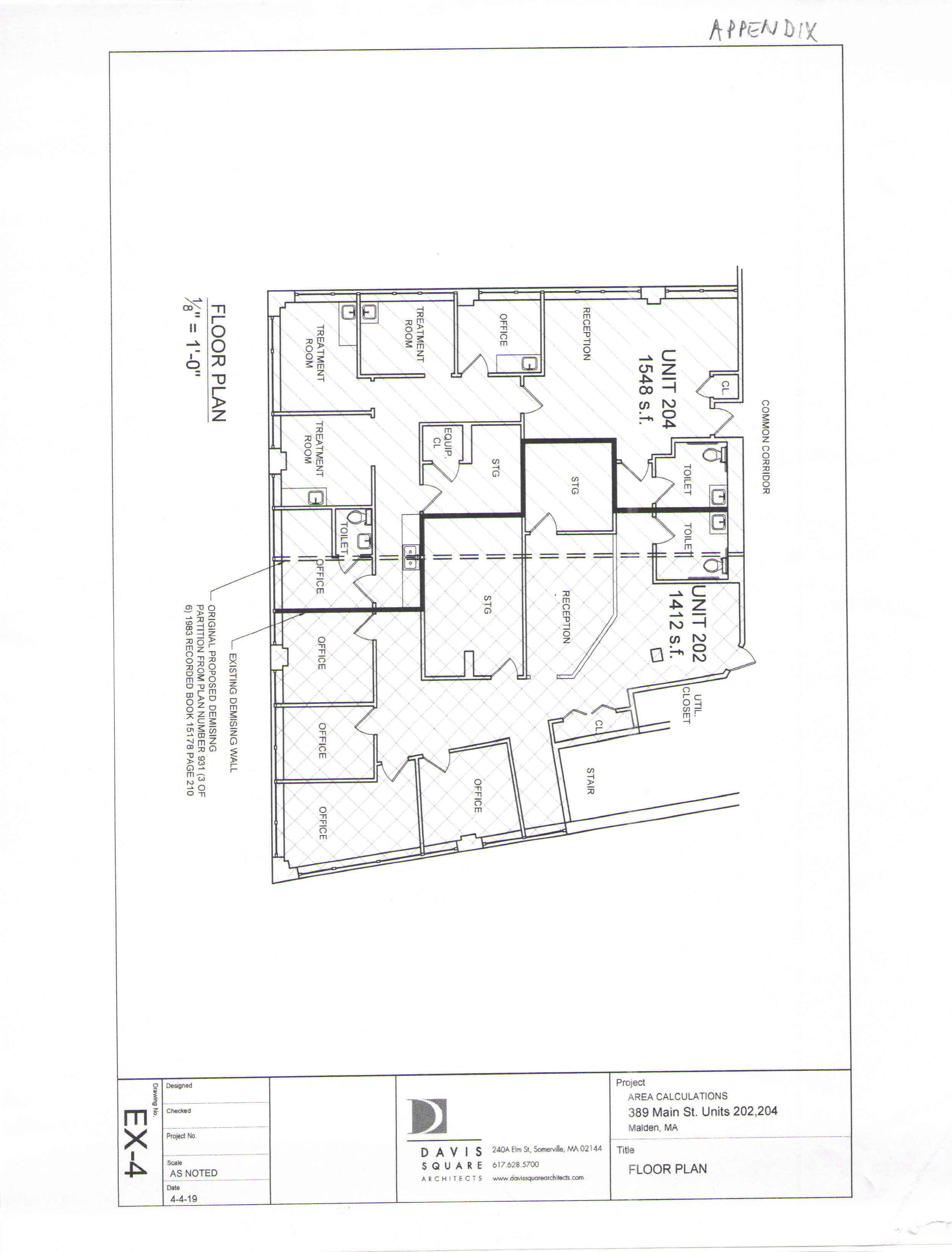

9. Section 5(c) of the Master Deed further provides:

[T]he Declarant may convey two or more adjacent Units to the same Unit Owner prior to the actual construction of the interior walls to be located on such broken lines noted in (b) above and, if such Unit Owner so elects by notation on the unit deed(s) conveying such adjacent Units from the Declarant to such Unit Owner, such interior walls shall not be constructed but such Units shall constitute separate Units which shall be deemed for all purposes to have been connected pursuant to the provisions of Section 13 . . . (and shall be governed in all relevant respects by said Section 13) and shall be capable of being partitioned into separate Units as provided in Section 13(g) . . . , or subdivided and combined as provided in Section 14(h) . . . , as fully and completely as though all common walls intended to be located on such broken lines had been actually constructed prior to the first conveyance of such Units by the Declarant.

10. In November 1983, the Condominium's "Declarant" conveyed to Family Service Association of Greater Boston the Disputed Units. Family Service's deed (included in Trial Exhibit 33, starting at page 80) is recorded at the Registry. The deed recites the Disputed Units' beneficial interests; they match the percentages on Exhibit B. The deed also says this: "Pursuant to Section 5(c) of the Master Deed, [Family Service] hereby declares that Units 201 and 202 shall constitute separate Units which shall be deemed to have been combined in accordance with the provisions of Section 13 of the Master Deed."

11. In 1992, the Condominium Trustees recorded an amendment to the Declaration of Trust (the "1992 Trust Amendment"). The Amendment deleted a sentence in the Declaration that said:

The Unit Owners shall be liable for common expenses and entitled to common profits of the Condominium in proportion to their respective percentages of beneficial interests as set forth in the Master Deed.

The 1992 Trust Amendment replaced that sentence with this:

The Unit Owners shall be liable for common expenses and entitled to common profits of the Condominium in proportion to the allocable share of such Unit Owner's Unit(s) of the total building rentable square footage contained within the Condominium. The total rentable square footage of the Condominium is 28,060 feet. . . .

The 1992 Trust Amendment presents the "Allocated Rentable Square Footage" of each Unit. The Amendment states that the "resulting percentage" for Unit 201 (which was then combined with Unit 202) is 12.8%, and then-Unit 204's resulting percentage is 5.7%. The Amendment doesn't purport to alter, however, any unit's beneficial interest in the Condominium.

12. In June 1999, Family Service sold to Marsupial Limited Partnership the Disputed Units. Marsupial's deed (included in Trial Exhibit 33, starting at page 95) is recorded at the Registry. The deed recites the Disputed Units' beneficial interests; they again match the percentages on Exhibit B. The deed also states that the Units are "conveyed together with the benefit of, and subject to, . . . the Master Deed . . . and all matters of record stated or referred to in the Master Deed as completely as if each were fully set forth herein. . . . Said premises are [also] conveyed subject to any and all matters of record insofar as now in force and applicable."

13. Linda Guild is one of Mystery's principals. In 1999, Guild was working for Guild Associates ("GA"). In 1999, GA asked to rent from Marsupial a portion of the Disputed Units. At the time GA first contacted Marsupial, the Disputed Units were still one physical space. GA didn't want all that space. Marsupial addressed that concern by proposing to build the Demising Walls. It did so in 1999, with GA's input as to where the Walls should go. After the Walls were built, GA coordinated the further fitting out of its leasehold, which corresponds with what Mystery today considers to be Unit 202.

14. A floor plan depicting today's Disputed Units (taken from Trial Exhibit 22) is attached as an Appendix to this decision. As one can see from the Appendix, the Demising Walls don't follow the Deeded Boundary. The Demising Walls give the occupants of Unit 202 access to a larger area than the Master Deed originally provided, and shrank the accessible area originally provided to Unit 204 under the Master Deed. [Note 2] And contrary to what § 5(b) of the Master Deed requires (see Finding #8 above), no "floor plan showing actual construction" nor a special amendment to the Master Deed was recorded in 1999.

15. In 2003, Marsupial conveyed the Disputed Units (Demising Walls and all) to Breton. Marsupial's deed to Breton (the "2003 Deed," included in Trial Exhibit 33, starting at page 111) is recorded at the Registry. The deed recites the Disputed Units' beneficial interests; they again match the percentages on Exhibit B. The deed repeats the language quoted in Finding #12 above.

16. In May 2004, an Amendment to Master Deed (the "2004 Master Deed Amendment") was recorded at the Registry. The Amendment states that Breton owned Units 201 and 202, and that Phillip K. Burgess, the trustee of the Breton Realty Trust (and the manager of Breton), owned Unit 204. The Amendment states that Breton and the Breton Realty Trust wished to "re-assign two of the Unit Numbers, so that the existing Unit 204 becomes Unit 201, and the existing Unit 201 becomes Unit 204."

17. The 2004 Master Deed Amendment also tried to do more than reassign unit numbers. The 2004 Master Deed Amendment states:

Exhibit B to the Master Deed shall be amended as to Units 201 and 204 only as follows:

a. Unit 201 2nd Floor 1,310 s.f. 5.7%

b. Unit 204 2nd Floor 1,569 s.f. 12.8%

18. The 2004 Master Deed Amendment had two defects. First, the numbers in the far-right column in Finding #17, under what Exhibit B calls "Percentage Interest," don't match any of the numbers in original Exhibit B (see Finding #7). Instead, the numbers correspond to those listed as "resulting percentages" in the 1992 Trust Amendment. That amendment changed only the Trust's method of allocating the common expenses and common profits of the Condominium: it didn't change any unit's beneficial interests in the Condominium, as set forth on Exhibit B.

19. The second defect in the 2004 Master Deed Amendment is that, while it recites that it was signed by unit owners holding 75% of the beneficial interests in the Condominium, it lacked the signature of the owner of Unit 203. Under § 17(a)(iii) of the Master Deed, "[n]o instrument of amendment which alters the percentage of the undivided interest to which any Unit is entitled in the common areas and facilities shall be of any force or effect unless the same has been signed by all Unit Owners . . . ." See also G.L. c. 183A, § 5 (alteration of a unit's percentage of undivided interests in a condominium requires the consent of all unit owners).

20. Because the 2004 Master Deed Amendment didn't receive the consent of all Condominium unit owners, it changed only the names of original Units 201 and 204. It didn't change the Disputed Units' beneficial interests in the Condominium. They remained as listed in the original Exhibit B.

21. In July 2004, Mystery (an LLC formed by members of the Guild family) purchased Unit 202 from Breton, pursuant to a unit deed (the "2004 Mystery Deed"). After buying Unit 202, Mystery leased the premises to GA.

22. The 2004 Mystery Deed is recorded at the Registry. It states that "[t]he Unit is shown on floor plans recorded simultaneously with the Master Deed," even though the Demising Walls had been built, and even though those Walls weren't on the Deeded Boundary. As one can see from the Appendix, if read literally, the 2004 Mystery Deed conveyed to Mystery an area that was behind two Demising Walls (and from all appearances, part of Breton's retained Unit 204). The 2004 Mystery Deed also didn't convey (if read literally) areas that now comprise half of the only bathroom in Mystery's suite, part of one of suite's hallways, part of the suite's reception area, an entire storage closet in the suite, and a portion of another storage room in the suite. The 2004 Mystery Deed also states that Breton was conveying Unit 202 together with only "[a]n undivided 5.8148% percent [sic] interest in common areas, facilities and elements of the Condominium" - the percentage that Exhibit B associated with Unit 202 in its original form.

23. The 2004 Mystery Deed further states:

Grantee, by accepting and recording this Deed and by executing this Deed in the space provided below, hereby acknowledges and agrees that . . . the owners of adjacent Units shall have the right to connect and/or subdivide and combine such Units in accordance with the provisions of Sections 5(c), 13, and 14 of the Master Deed, respectively. . . . Grantee further agrees that Grantee's acceptance and recording of this Deed and execution of this Deed . . . shall constitute Grantee's consent to the exercise of any such rights described above and to any amendment of the Master Deed made in connection with any exercise of such rights. The various acknowledgments and agreements set forth above shall apply to any exercise of the rights enumerated above which occurs either before or after the recording of this Deed. . . .

Further still, Grantee, by accepting and recording this Deed, and by executing this Deed . . . , hereby appoints and constitutes the Trustees of the Condominium Trust, and their respective successors, and each of them acting singly, with full power of substitution, as Grantee's true and lawful proxy and attorney-in-fact with full power coupled with an interest which cannot be revoked, to vote for, execute, acknowledge, deliver and record one or more amendments to the Master Deed pursuant to any of the above referenced provisions, and one or more amendments to the Declaration of Trust necessitated by such amending of the Master Deed. To the greatest extent permissible by law, the power of attorney granted herein shall also be binding upon all future owners of the Unit with the result that all such future owners of the Unit shall be deemed to have granted a similar power of attorney to the Trustees of the Condominium Trust.

24. At the time Mystery received the 2004 Mystery Deed, Mystery granted Eastern Bank a mortgage (the "Unit 202 Mortgage"). The description of the mortgaged premises in the Unit 202 Mortgage matches the description of Unit 202 contained in the 2004 Mystery Deed. [Note 3]

25. At the time of execution of the 2004 Mystery Deed, Unit 202 was still a "Connected Unit" with Unit 204 for purposes of the Master Deed. Breton's 2004 sale of Unit 202 thus implicated three provisions of the Master Deed:

Section 13(f), which provides: "At such time as Connected Units are no longer to be in common ownership . . . , the owner(s) of such Units shall promptly restore the common walls and/or floors. . . ."

Section 13(g), which provides: "Any Unit Owner owning Connected Units . . . may partition such Connected Units into separate Units by constructing such common walls . . . as are shown by broken lines on the [Floor Plans] for such Units. . . ."

And § 14(h), which provides (emphasis added):

If a Unit Owner owning Connected Units desires to subdivide and combine such Connected Units so as to create new separate Units which are different in size or layout from the size and layout of the original separate Units which comprise such Connected Units, such Unit Owner may do so pursuant to this Section 14. . . . In such a case, for purposes of making the calculations of new percentage interests provided in Section 14(f) . . . , the Subdivided Unit and the Expanded Unit (which formerly comprised such Connected Units) shall be deemed to have had the same size and layout as existed prior to such Units having become Connected Units or if such Units became Connected Units pursuant to Section 5(c) . . . , the same size and layout as is shown on the [Floor Plans].

26. Breton did not "restore" Unit 202 to the dimensions shown in the Master Deed. Breton also did not partition the Disputed Units in accordance with § 13(g) of the Master Deed. Thus, because the Devising Walls created a "different . . . size or layout" for the Disputed Units from those shown on the Floor Plans, § 14(h) of the Master Deed (and, by extension, § 14 of the Master Deed, entitled "Subdivision and Combining of Units") governed Breton's responsibilities in connection with its sale to Mystery of purported Unit 202.

27. But Breton didn't comply with § 14 either, at least not in 2004. Section 14 provides (emphasis added):

A Unit Owner may subdivide . . . his Unit (such Unit hereinafter called the "Subdivided Unit") for the purpose of selling a portion thereof to the owner of an adjacent Unit on the same floor but for no other purpose and a Unit Owner may purchase and combine . . . with his Unit so as to create a single larger Unit (such Unit hereinafter called the "Expanded Unit") any such subdivided portion of an adjacent Unit, provided that such subdivision and combining of a subdivided portion of the Subdivided Unit with the Expanded Unit shall be effected only in accordance with the following terms and conditions:

. . .

(b) A deed from the owner of the Subdivided Unit conveying to the owner of the Expanded Unit the portion of the Subdivided Unit to be combined with the Expanded Unit shall be recorded in the Registry of Deeds together with (i) a new plan of the Subdivided Unit and Expanded Unit after such subdivision and combining . . . has been completed (such Units collectively called the "Resulting Units") (which plan shall show the layout of Resulting Units and bear the same verified statement of a registered architect, registered professional engineer or a registered land surveyor as is required by . . . Chapter 183A in connection with the unit plan which is part of any first unit deed and also the same verified statement as is required by Chapter 183A in connection with [the Floor Plans]) and (ii) a certificate signed by at least two Trustees stating that all such work has been performed in accordance with this Section 14 and setting forth the new respective percentage interests of the Resulting Units. Such new

plan and certificate . . . shall be recorded as a special amendment to this Master Deed pursuant to Section 17(b)(iii). . . .

And § 17(b)(iii) of the Master Deed provides:

In the event any Units are subdivided and combined as described in Section 14 . . ., upon completion of such work, this Master Deed shall be amended by an instrument in writing (1) signed and acknowledged by the Unit Owner(s) of such Units and also signed and acknowledged either (A) by the owners of all of the other Units in the Condominium or (B) by a majority of the Trustees, as attorneys for such owners of the other Units pursuant to the Power of Attorney to be contained in the deed by which the Declarant conveys each Unit to any third party purchaser and also to be contained in all other deeds of any of the Units . . . , and (2) duly recorded with the Registry of Deeds. Such instrument shall state the new respective percentage interests of the Expanded Unit and the Subdivided Unit and there shall be attached to such instrument the plan of the Expanded Unit and the Subdivided Unit and certificate of the Trustees as required by Section 14(b). . . .

Breton took no steps to deliver or record any of the things described in §§ 14(b) and 17(b)(iii) of the Master Deed until 2007.

28. Dr. Liu became interested in purchasing Breton's remaining unit, Unit 204, in the fall of 2006. She sought a Malden location to relocate her dental practice. She had bought and sold other real estate previously, including other real estate in Malden. She also had purchased a condominium unit once before. She hired attorneys to assist her with those transactions.

29. Dr. Liu signed a purchase and sale agreement with Breton in September 2006 (the "P&S"). Breton agreed in the P&S to convey the same Unit 204 it had received in the 2003 Deed, together with "an undivided 6.6842% . . . interest" in the Condominium and its common areas (the same percentage Exhibit B allocates to Unit 201/204 in its original form). [Note 4] Liu didn't review the Master Deed or the Floor Plans before signing the P&S.

30. Under the P&S, the closing was to be December 8, 2006.

31. Paragraph 13 of the P&S states: "The acceptance of a deed by [Dr. Liu] shall be deemed to be a full performance and discharge of every agreement and obligation herein contained or expressed, except such as are, by the express terms hereof, to be performed after the delivery of said deed."

32. The P&S identified attorney Deborah L. Miller as Breton's attorney, one required to receive copies of all notices under the P&S. The P&S identified no attorney for Dr. Liu. Sometime after signing the P&S, Liu hired attorney Arlene Fothergill to represent Liu in her purchase of Unit 204.

33. The parties twice amended the P&S. One of the amendments changed the closing date to January 8, 2007. The other amendment isn't material to this dispute.

34. Dr. Liu entered modified Unit 204 at least twice before the closing of her purchase of the unit. One visit occurred before she signed the P&S, and the other visit occurred after. On one of the visits, she was accompanied by an inspector she'd hired. At the time of both of her visits, the Demising Walls, the ceilings abutting those walls, Unit 204's lighting, its exterior windows, and its HVAC systems were as they appeared at the time of trial.

35. At some point, attorney Fothergill ascertained that the apparent Unit 204 differed from the unit shown in the Master Deed. Fothergill learned of other discrepancies as well. (Fothergill died sometime before the trial of this case. Findings ##47-49 explore how she may have discovered Unit 204's problems, but the Court can't determine from the trial record how she actually learned of them.) A facsimile that Fothergill sent to attorney Miller early in the afternoon of Friday, January 5, 2007 summarizes what Fothergill detected:

Good morning Debra,

The deed you sent over does not include any square feet and the % interest is only 5.7%.

Attached please find:

1. The listing agreement showing 1569 s.f. and total 1601 s.f.;

2. Exhibit B of the Master Deed showing unit 204 (201) 1,569 s.f. and 6.6842% interest;

3. Unit deed to Breton LLC unit 204 (201) 6.6842% interest and Unit 202 - 5.8148%

4. The plan for unit 204 (201) with a dot[t]ed line separating it from unit 202;

5. 2004 Amendment to Master [D]eed changing unit 201 to 204 & showing 12.8% interest and 1,569 s.f. at this time 204 (201) & 202 are combined;

6. Trustee's Certificate Regarding Amendment to Decl. of Trust shows unit 201 12.8% interest;

7. Unit deed conveying unit 202 grants 5.8148% interest; and not indicating any s.f.;

. . .

Also, when Dr. Liu sent a contractor over for the fit-up he found a discrepancy of about 200 s.f.

There are so many discrepancies that I need a[n] Amendment to Master deed, in accordance with the Master deed . . . with a plan showing the s.f. and % interest. I won't be able to obtain title insurance without an exact s.f. and % of interest. . . .

36. By later that same afternoon, attorney Fothergill had concluded that the Monday, January 8, 2007, closing shouldn't occur. Fothergill faxed this to attorney Miller (also included in Trial Exhibit 23):

This is to confirm that I cannot close on the above referenced property on Monday until there is an Amendment to the Master Deed and a new plan of unit 204. Please inform your client. I left a message for the R.E. Broker . . . that an extension is needed. I also left a message for Dr. Liu that I could not close on Monday and extension would be needed. The length of the extension would be dependent on how long is needed to obtain the plan and Amendment to the Master Deed. . . .

37. On February 27, 2007, the closing of the sale of purported Unit 204 occurred. Dr. Liu and attorneys Miller and Fothergill attended the closing. The following day, three documents were recorded at the Registry, prior to the recording of Liu's Unit Deed: (a) a Special Amendment to Master Deed (the "2007 Special Master Deed Amendment"); (b) an Amendment to Master Deed (the "2007 Regular Master Deed Amendment"); and (c) an "Amendment to Condominium Trust" (the "2007 Trust Amendment"). Miller prepared the documents identified in this Finding. This Decision will refer to the documents collectively as the "Four Documents," and the three amendments collectively as the "2007 Amendments."

38. The signatories to the 2007 Special Master Deed Amendment were Breton (the record owner of Unit 204 prior to its conveyance to Dr. Liu), Mystery (the record owner of Unit 202), and two of the Condominium Trust's trustees.

39. The 2007 Special Master Deed Amendment recites that Breton, Mystery, and the two Condominium Trustees who signed the Amendment

state that Units 202 and 204 were divided as shown on the plan entitled "Condominium Floor Plan for the City Center Condominium 389 MainStreet [sic] Malden Mass." Prepared by Medford Engineering & Survey dated January 23, 2007, recorded herewith [the "2007 Floor Plan"]. Pursuant to Section 13(a) of the Master Deed . . ., the Trustees hereby certify that all such work has been performed in accordance with said Section 13 of the Master Deed. This instrument constitutes a Special Amendment in accordance with Section 17(b)(ii) of the Master Deed.

40. Ms. Guild signed on Mystery's behalf the 2007 Special Master Deed Amendment. Guild signed because the Condominium's building manager asked her to do so. Guild provided no testimony that she or Mystery took any steps in reliance on the Amendment.

41. The 2007 Special Master Deed Amendment did not comply with § 14 of the Master Deed. That's because:

Ignoring the requirements of §§ 14(b)(i) and 17(b)(iii) of the Master Deed, the 2007 Floor Plan does not "show the layout of Resulting Units. . . ." It depicts only the layout of Unit 204 (Dr. Liu's unit), and not Unit 202 (Mystery's unit). The 2007 Floor Plan does show, however, the Demising Walls.

Ignoring the requirements of § 14(b)(ii) of the Master Deed, the 2007 Special Master Deed Amendment does not contain a certification that "all such work has been performed in accordance with . . . Section 14. . . ." Instead, the Amendment recites only that the work had been done in accordance with Section 13.

Ignoring the requirements of §§ 14(b)(ii) and 17(b)(iii) of the Master Deed, the 2007 Special Master Deed Amendment does not "set[] forth the new respective percentage interests of the Resulting Units." (As will be seen in Findings #43 and #51 below, other documents purport that modified Unit 204 has a 5.6% beneficial interest in the Condominium.)

Ignoring the requirements of § 17(b)(iii) of the Master Deed, the 2007 Special Master Deed Amendment was not "signed and acknowledged either (A) by the owners of all of the other Units in the Condominium or (B) by a majority of the Trustees, as attorneys for such owners of the other Units. . . ." Only two of the Unit Owners (Breton and Mystery), and only two (less than a majority) of persons purporting to be Condominium Trustees, signed the Amendment. To make matters worse, at the time they signed the 2007 Special Master Deed Amendment, neither of the two purported Trustees had been duly appointed as trustees. See Declaration of Trust, § 3.1(A) (appointment becomes effective upon the recording of a certificate of appointment signed by the person appointed and by any two unit owners or trustees, who must certify that the person appointed was elected by unit owners holding no less than 51% of the beneficial interests).

42. The 2007 Special Master Deed Amendment also did not receive the assent of Mystery's mortgagee, Eastern Bank.

43. The 2007 Regular Master Deed Amendment was defective too. It recites that the 2004 Master Deed Amendment "contained a typographical error in which the percentage interest assigned to Unit 204 was listed as 12.8%". The 2007 Regular Master Deed Amendment asserts that "the actual percentage interest for Unit 204 should be 5.6%," and purports to change Unit 204's interest to 5.6%. The parties have stipulated, however, that not all of the Condominium's unit owners signed the 2007 Master Deed Amendment. See Agreed Finding of Fact #35. The 2007 Regular Master Deed Amendment thus was ineffective under § 17(b)(iii) of the Master Deed, and it didn't change the Disputed Units' beneficial interests in the Condominium.

44. The third of the Three Amendments is the 2007 Trust Amendment. It states that the 1992 Trust Amendment "indicated that Unit 201 contained 3,578 s.f. with a resulting 12.8 percentage interest in the condominium," but "did not indicate that Unit 201 (now known as Unit 204) and 202 had a combined square footage of 3,578 [sic] with a combined percentage interest of 12.8%." (Recall from Finding #11 above that the 1992 Trust Amendment didn't change anyone's "percentage interest" in the Condominium; it changed only the formula for allocating common expenses and profits.) The 2007 Trust Amendment further asserts that "Unit 201 (now known as Unit 204) as divided from Unit 202 contains 1,320 usable square feet (1,571 rentable square feet) with a resulting 5.6 percentage interest. . . ." The 2007 Trust Amendment then asserts that "Unit Owners holding [75%] of the beneficial interest in the Condominium" had thus authorized the Trustees to amend the Declaration of Trust "to show that Unit 204 (formerly known as Unit 201) contains 1,320 usable square feet (1,571 rentable square feet) with a resulting percentage interest of 5.6." [Note 5] Seven people signed the 2007 Trust Amendment, purportedly in their capacities as Condominium Trustees.

45. No one directly associated with the Unit 204 closing, other than Dr. Liu, testified at trial. That includes Breton's manager, Mr. Burgess; Breton's attorney, attorney Miller; and the deceased attorney Fothergill.

46. The Court finds that at the time of the Unit 204 closing, attorney Fothergill was aware of the contents of the Four Documents. The Court also finds that Breton knew, at the time of the closing, that Fothergill had reviewed the Four Documents. The Court makes these findings based on the evidence discussed in Findings ##47-49 below.

47. The as-recorded versions of the 2007 Special Master Deed Amendment, the 2007 Regular Master Deed Amendment, and Dr. Liu's Unit Deed bear on their first page, in the bottom margin, a stamp:

Law Office Arlene J. Fothergill

61 Main Street

Stoneham MA 02180

The as-recorded copy of the 2007 Trust Amendment bears on its first page, in the bottom margin, in handwriting that appears to be Fothergill's:

Arlene Fothergill

61 Main St

Stoneham MA 02180

48. The Court infers from the margin notes that attorney Fothergill had seen the final versions of the Four Documents and wanted as-recorded copies returned to her. Dr. Liu suggested at trial that someone might have added the notes after the fact, or without Fothergill's knowledge. The Court disagrees. The parties offered at trial, as an agreed exhibit, Trial Exhibit 33. The exhibit is Fothergill's closing file, accompanied by an affidavit from Fothergill in which she swears that the documents comprise the entire file. Several items in file show that Fothergill supervised the recording of the Four Documents:

Page 199 of Trial Exhibit 33 is an invoice from Ms. Janice Jones, a person whose name also appears in the file as having conducted a title examination for Unit 204. The invoice at page 199 is for extra fees Jones incurred in recording the Four Documents, along with a Registry receipt. Trial Exhibit 33 also contains at pages 203-204 a check from Fothergill to Jones for her invoice; on the check, Fothergill wrote "Liu - Recording Plan."

Pages 236-255 and 257-261 of Trial Exhibit 33 are as-recorded copies of the Four Documents, as well as other documents recorded simultaneously with them. On page 232, a handwritten note appears on a copy of the settlement statement for the closing of Unit 204. The note says, "Dr. Lui[ [Note 6]] stuff back from the Registry" and bears a March 22, 2007 date.

49. Trial Exhibit 33 also contains what appears to be Ms. Jones's title examination. Page 2 of what appear to be her notes (page 44 of Trial Exhibit 33) says: "Query need for Condo Docs to be amended if Units 201 + 202 are no longer combined." Page 200 of Trial Exhibit 33 is handwritten notes that appear to pertain to what had been recorded concerning the Disputed Units prior to 2007. Some of the numbers that appear in those notes reappear in the first of Fothergill's January 5, 2007 facsimiles to attorney Miller (see Finding #35 above). The notes include the word "Problem".

50. Dr. Liu testified that attorney Fothergill didn't tell Liu that (a) the Demising Walls weren't on the Deeded Boundary; (b) following construction of the Demising Walls, Unit 204 had less area than described in Exhibit B to the Master Deed and in the P&S; or (c) the Three Amendments were being executed and recorded prior to the recording of Liu's Unit Deed. Liu also claimed that Fothergill didn't explain the purpose of the Three Amendments. The Court makes no finding as to whether Liu's testimony about her attorney's non-disclosures is true. That's because Fothergill knew of the Four Documents prior to the Unit 204 closing, and allowed the closing to proceed: indeed, Fothergill made the recording of the Three Amendments a prerequisite to closing. As explained later in this Decision, under Massachusetts law, Fothergill's knowledge is attributed to Liu, regardless of Liu's actual knowledge. It is thus unnecessary for the Court to make any findings concerning what, if anything, Fothergill communicated to Liu concerning the Four Documents to answer the issues designated for trial. See Joseph R. Nolan and Bruce Henry, 9 M.P.S.§ 36.7 (2004) (court need not make rulings predicated on fragmentary evidence, or on questions that do not decide the issues for trial).

51. Dr. Liu's Unit Deed, the fourth of the Four Documents, states that Breton is conveying Unit 204 as "shown on floor plans recorded simultaneously with the Master Deed." The Unit Deed also states that the Unit is conveyed together with "[a]n undivided 5.6% . . . interest in common areas, facilities and elements of the Condominium as described in the Master Deed." (Emphasis added.) The Unit Deed says the Unit "is conveyed subject to . . . [t]he provisions of the Master Deed (and the floor plans of the Condominium recorded simultaneously with and as a part of the Master Deed), and the Declaration of Trust, as they may be amended from time to time by instrument recorded with said Deeds. . . ."

52. Dr. Liu's Unit Deed also contains two paragraphs that also appear in the 2004 Mystery Deed:

Grantee, by accepting and recording this Deed and by executing this Deed in the space provided below, hereby acknowledges and agrees that . . . the owners of adjacent Units shall have the right to connect and/or subdivide and combine such Units in accordance with the provisions of Sections 5(c), 13, and 14 of the Master Deed, respectively. . . . Grantee further agrees that Grantee's acceptance and recording of this Deed and execution of this Deed . . . shall constitute Grantee's consent to the exercise of any such rights described above and to any amendment of the Master Deed made in connection with any exercise of such rights. The various acknowledgments and agreements set forth above shall apply to any exercise of the rights enumerated above which occurs either before or after the recording of this Deed. . . .

Further still, Grantee, by accepting and recording this Deed, and by executing this Deed . . . , hereby appoints and constitutes the Trustees of the Condominium Trust, and their respective successors, and each of them acting singly, with full power of substitution, as Grantee's true and lawful proxy and attorney-in-fact with full power coupled with an interest which cannot be revoked, to vote for, execute, acknowledge, deliver and record one or more amendments to the Master Deed pursuant to any of the above-referenced provisions, and one or more amendments to the Declaration of Trust necessitated by such amending of the Master Deed. To the greatest extent permissible by law, the power of attorney granted herein shall also be binding upon all future owners of the Unit with the result that all such future owners of the Unit shall be deemed to have granted a similar power of attorney to the Trustees of the Condominium Trust.

53. In 2015, eight years after buying purported Unit 204, Dr. Liu conveyed to herself, as Trustee of the 389 Main Street Trust, whatever interest in Unit 204 she acquired in her 2007 Unit Deed. The 2015 deed uses the same description of Unit 204 that appears in her 2007 Unit Deed. The 2015 deed also states (as did her 2007 Unit Deed) that she was conveying a 5.6% beneficial interest in the Condominium.

54. On July 2, 2020, Breton and Mystery executed a confirmatory deed, in favor of Mystery (the "Confirmatory Deed," attached as Exhibit A to Appendix to Statement of Facts in Support of Defendants' Joint Motion for Summary Judgment, docketed July 13, 2020 ("Exhibit A")). The Confirmatory Deed states that while the 2004 Mystery Deed says that Unit 202 "is shown on floor plans recorded simultaneously with the Master Deed," those floor plans "did not accurately describe the square footage granted to Mystery, LLC." The Confirmatory Deed states that the "correct square footage . . . is now shown on the Davis Square Architects Floor Plan, dated: April 4, 2019 simultaneously recorded with this Confirmatory Deed, which represents the size and layout of the Unit at the time of the original conveyance to Mystery LLC." The Confirmatory Deed contained in Exhibit A doesn't have any plans attached to it. The Registry's online records also do not show any recording of the Confirmatory Deed. The Confirmatory Deed nevertheless asserts that Breton has conveyed to Mystery Unit 202 together with an "undivided 6.98% . . . interest in common areas facilities and elements of the Condominium as described in the Master Deed." (Emphasis added.)

55. Since acquiring purported Unit 204, Dr. Liu's property taxes have been calculated as if she owned Unit 204 as described originally in the Master Deed, meaning that she has been taxed for areas that are on Mystery's side of the Devising Walls. It is not clear from the trial record how the Condominium Association has been calculating Dr. Liu's share of condominium fees since February 2007, or whether those calculations assume Dr. Liu has possession of the entirety of Unit 204 as described originally in the Master Deed.

* * *

A condominium's master deed prescribes "the rules of the game" within a condominium. Straus v. Oyster River Condominium Trust, 417 Mass. 442 , 452 (1994). The parties agree that Breton didn't abide by those rules when it sold purported Unit 202 to Mystery in 2004, or when Breton sold purported Unit 204 to Dr. Liu in 2007. Liu argues that, as a result, (a) Mystery owns only Unit 202 as described originally in the Master Deed; (b) Liu owns Unit 204 as described originally in the Master Deed; and (c) Mystery should be ordered to remove the Demising Walls, rebuild them along the Deeded Boundary, and stay out of Unit 204. See Peters v. Archambault, 361 Mass. 91 , 92 (1972) ("In Massachusetts a landowner is ordinarily entitled to mandatory equitable relief to compel removal of a structure significantly encroaching on his land, even though the encroachment was unintentional or negligent and the cost of removal is substantial in comparison to any injury suffered by the owner of the lot upon which the encroachment has taken place"); Xifaras v. Andrade, 59 Mass. App. Ct. 789 , 794-795 (2003) (applying Peters rule to encroachments between condominium units). [Note 7] Liu also seeks declarations as to (x) the location of the boundary between the Disputed Units, (y) the extent of Mystery's interests in areas comprising the original layout of Unit 204, and (z) Unit 204's beneficial interests in the Condominium.

In response, Defendants make an equitable argument: that regardless of Breton's errors, in 2007 Dr. Liu bought the Unit 204 she expected to buy, the modified unit demarcated by the Demising Walls. And while Defendants concede that several Condominium documents are ineffective, in the end Defendants insist the Demising Walls should be left alone. [Note 8]

Defendants' equitable defenses posed three issues for trial: (1) whether Dr. Liu had actual or constructive knowledge, at the time she accepted her 2007 Unit Deed, that Unit 204's physical layout differed from the layout in the Master Deed; (2) if so, whether she should be estopped from raising her claims in this action; and (3) if she knew of the different layout at the time of the 2007 closing, whether she has waived her claims for relief in this action. The Court addresses each issue in turn.

Dr. Liu's Knowledge. Under Massachusetts law, an attorney's knowledge of facts pertaining to a real-estate transaction are properly imputed to his or her client. See, for example, Quinn v. Hintlian, 4 Mass. App. Ct. 805 (1976) (rescript); One-O-Six Realty, Inc. v. Quinn, 66 Mass. App. Ct. 149 , 154 (2006). See also Flynn v. Wallace, 359 Mass. 711 , 717 (1971) (knowledge of buyer's agent is imputed to buyer); Sunrise Properties, Inc. v. Bacon, Wilson, Ratner, Cohen, Salvage, Fialky & Fitzgerald, P.C., 425 Mass. 63 , 67 (1997) (knowledge of agent is imputed to agent's principal). Once a client is charged with knowledge of particular facts, he or she "is likewise properly charged with their correctly interpreted legal effect. That is to say, we decline to apply a subjective standard to consider whether the [client] correctly understood [the implications of the facts], rather than an objective standard charging the [client] with knowledge of the actual legal effect of [those facts]." One-O-Six, 66 Mass. App. Ct. at 154- 155.

That a lawyer may have misadvised his or her client, or even not told the client important facts, does not relieve the client vis à vis other persons of the knowledge the law imputes to the client. For better or worse, under Massachusetts law, "[a] client is bound by the mistakes of its counsel." Id. at 155; see also Massachusetts Parole Bd. v. Civ. Serv. Comm'n, 47 Mass. App. Ct. 760 , 766 (1999) ("[O]rdinarily, a person is held accountable for the conclusions of his attorney to the extent that one accedes to those conclusions or permits counsel to act in one's stead"). Attorney Fothergill understood by January 5, 2007 that Breton couldn't deliver good title to the Unit 204 described in the P&S. She also understood that Breton couldn't deliver title to modified Unit 204 unless the Master Deed were amended. She alerted Breton to these issues. Instead of promising to perform in the manner the P&S dictated (that is, deliver title to Unit 204 as described in the original Master Deed), Breton proposed to tender alternative performance (that is, deliver title to modified Unit 204) at the postponed February 2007 closing. Yes, the unit deed that Breton proposed to tender to Dr. Liu said (consistent with the P&S) that Breton was conveying Unit 204 "as described in the Master Deed," but Fothergill understood that Breton would be recording the Three Amendments before the unit deed was recorded. Fothergill also understood that had the Three Amendments been properly drafted and approved, they would have changed the boundaries of Unit 204 as they appeared in the original Master Deed, along with the Unit's beneficial interests in the Condominium.

Attorney Fothergill thus had a choice in early 2007: counsel Dr. Liu to terminate the P&S or advise her to accept alternative performance. The record shows that Liu, knowingly or not, but with her attorney at her side, chose the second option. Under ¶ 13 of the P&S, Liu's acceptance of a deed is "deemed to be a full performance and discharge of every agreement and obligation herein contained or expressed, except such as are, by the express terms hereof, to be performed after the delivery of said deed." [Note 9] The Court thus holds that, taking Fothergill's knowledge and Liu's actions together, Liu agreed at the time of the February 27, 2007 closing to buy not the Unit 204 that the Master Deed originally described, but rather the Unit 204 as enclosed by the Demising Walls, provided that the Three Amendments were properly executed and recorded.

Estoppel. To estop Dr. Liu from bringing her claims in this action, Defendants must show "(1.) A representation or conduct amounting to a representation intended to induce a course of conduct on the part of the person to whom the representation is made. (2.) An act or omission resulting from the representation, whether actual or by conduct, by the person to whom the representation is made. (3.) Detriment to such person as a consequence of the act or omission." Turnpike Motors, Inc. v. Newbury Group, Inc., 413 Mass. 119 , 123 (1992), quoting Cleaveland v. Malden Sav. Bank, 291 Mass. 295 , 297-298 (1935).

Mystery claims that Dr. Liu's conduct "lulled and induced Mystery . . . into treating its unit as one having the square footage depicted on the [2007 Special Master Deed Amendment]." Mystery Trial Brief, 15 (Feb. 1, 2021). Mystery also contends that it made improvements to Unit 202 in reliance on the Amendment. See id. Mystery offered no testimony supporting either contention. [Note 10] The only evidence at trial about improvements to Unit 202 concerned ones made before Mystery took title to that unit in 2004. Liu didn't set foot in the Condominium until late 2006. [Note 11] The Court thus holds that Liu is not estopped from bringing her claims in this action.

Waiver. Waiver is the "intentional relinquishment of a known right." Nashua River Paper Co. v. Lindsay, 242 Mass. 206 , 208 (1922). "Waiver may occur by an express and affirmative act, or may be inferred by a party's conduct, where the conduct is 'consistent with and indicative of an intent to relinquish voluntarily a particular right [such] that no other reasonable explanation of [the] conduct is possible.'" KACT, Inc. v. Rubin, 62 Mass. App. Ct. 689 , 695 (2004), quoting Attorney Gen. v. Industrial Nat'l Bank, 380 Mass. 533 , 536 n.4 (1980). When a "waiver is not explicit, it must be premised on 'clear, decisive and unequivocal conduct'" that demonstrates both an intention to waive something and the scope of the alleged waiver. KACT, 62 Mass. App. Ct. at 695, quoting Glynn v. Gloucester, 9 Mass. App. Ct. 454 , 462 (1980). "Whether waiver exists is a question of fact . . . ." KACT, 62 Mass. App. Ct. at 695.

Defendants contend that because Dr. Liu knew (at least constructively) of Unit 204's title defects, yet closed on the 2007 transaction anyway, she has waived all of her claims in this action. Defendants' argument sweeps too far. Yes, Liu (through attorney Fothergill) agreed to accept a deed for modified Unit 204, and not insist that the Demising Walls be relocated. She thus waived her right to claim that Unit 204 has a different shape, or to have the Demising Walls moved, once she accepted her Unit Deed. But Fothergill's January 2007 correspondence with attorney Miller demonstrates that Liu's waiver was contingent on Breton delivering effective amendments to the Master Deed and the Declaration of Trust. Defendants failed to prove at trial that Liu and/or Fothergill knew of, but agreed to waive, the undisclosed defects in (and the deficient approvals of) the 2007 amendments. [Note 12]

The Court thus holds that, while Dr. Liu has waived her right to (a) obtain title to Unit 204 as described in the original, unamended Master Deed; (b) demand removal of encroaching Demising Walls; and (c) insist on construction of a wall solely on the Deeded Boundary, those waivers are contingent on effective amendments to the Master Deed and the Declaration of Trust. Those amendments must properly ratify the alterations to the Disputed Units, make lawful adjustments to the Units' beneficial interests, and fix the Declaration of Trust's provisions regarding those Units' obligations for common fees and expenses. The Court thus ORDERS the parties to appear for a telephonic status conference on April 20, 2021 at 12:00 noon, to discuss whether additional proceedings are necessary before the Court orders final remedies in this action.

SO ORDERED.

MANHUI LIU, Plaintiff, v. MYSTERY, LLC; and KRISTIN AMARAL, JOHNATHAN CHASE, LISA GALLATIN, DAVID HORNUNG, and HAMID R. TABRIZI, as Trustees of the City Center Office Condominium Trust, Defendants

MANHUI LIU, Plaintiff, v. MYSTERY, LLC; and KRISTIN AMARAL, JOHNATHAN CHASE, LISA GALLATIN, DAVID HORNUNG, and HAMID R. TABRIZI, as Trustees of the City Center Office Condominium Trust, Defendants